In-process research and development (IPR&D) acquired in a business combination is a crucial aspect of valuing and accounting for mergers and acquisitions. When one company acquires another, the acquiring company must allocate the purchase price to the identifiable assets acquired and liabilities assumed. This includes intangible assets like patents, trademarks, and crucially, IPR&D. Understanding how IPR&D is treated differs significantly from research and development conducted internally.

What is In-Process Research and Development (IPR&D)?

IPR&D refers to any research and development projects that are not yet completed at the time of a business combination. These projects are considered an intangible asset and are recognized at fair value as part of the acquisition accounting process. This is a key difference from internally generated R&D, which is generally expensed as incurred.

Accounting for IPR&D in a Business Combination

The accounting treatment for IPR&D is governed by accounting standards like IFRS 3 (International Financial Reporting Standards) and ASC 805 (US GAAP). These standards require the acquirer to recognize IPR&D as an intangible asset separately from goodwill. The fair value of IPR&D is typically determined using a discounted cash flow analysis, considering the expected future benefits derived from the ongoing research and development projects.

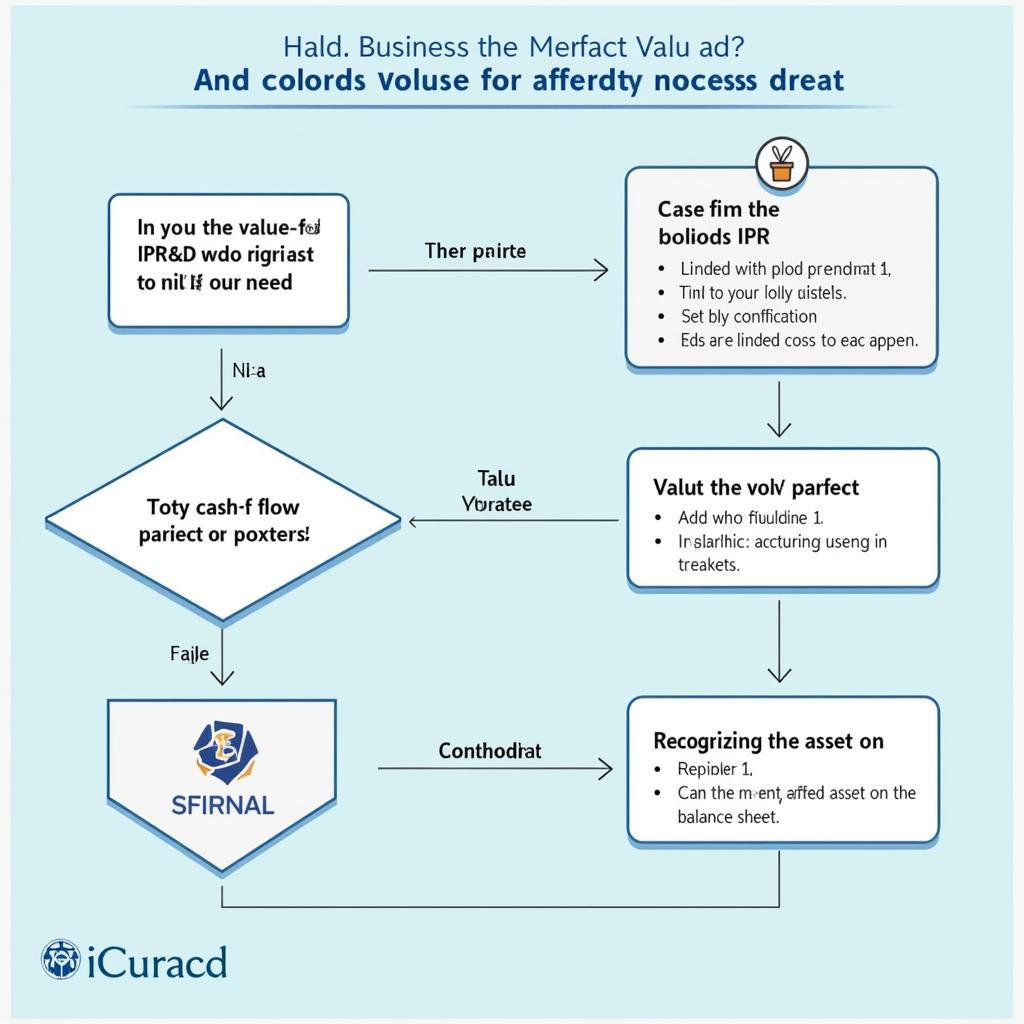

Key Steps in Accounting for IPR&D

- Identification: Identify all in-process research and development projects acquired.

- Valuation: Determine the fair value of each identified IPR&D project.

- Recognition: Recognize the IPR&D as an intangible asset at fair value.

- Amortization or Impairment: IPR&D is not amortized. Instead, it is tested for impairment annually or more frequently if indicators of impairment exist. If the fair value of the IPR&D falls below its carrying amount, an impairment loss is recognized.

IPR&D Valuation Process in a Business Combination

IPR&D Valuation Process in a Business Combination

Why is IPR&D Important in a Business Combination?

IPR&D can represent a significant portion of the purchase price in acquisitions, particularly in industries like pharmaceuticals, biotechnology, and technology. Properly accounting for and valuing IPR&D is essential for accurate financial reporting and for making informed investment decisions. Failing to adequately assess the value of IPR&D can lead to overpaying for an acquisition or misrepresenting the financial position of the acquiring company.

Impacts of IPR&D on Financial Statements

- Balance Sheet: IPR&D is recognized as an intangible asset, increasing the total assets of the acquirer.

- Income Statement: Impairment losses related to IPR&D are recognized on the income statement, potentially impacting profitability.

- Cash Flow Statement: Acquisition of IPR&D is reflected in the investing activities section of the cash flow statement.

Future of IPR&D in Business Combinations

As industries continue to invest heavily in research and development, the importance of IPR&D in business combinations is expected to grow. Advancements in valuation techniques and accounting standards will be necessary to accurately capture the value and risks associated with these intangible assets. Increased scrutiny from regulators and investors will also demand greater transparency and accuracy in reporting IPR&D.

“Accurate valuation of IPR&D is critical for making sound investment decisions in acquisitions,” says Dr. Emily Carter, a senior financial analyst specializing in M&A. “It’s not just about the numbers on the balance sheet, but understanding the potential these projects hold for future innovation and growth.”

Future Trends in IPR&D Acquisitions

Future Trends in IPR&D Acquisitions

Conclusion

In-process research and development acquired in a business combination represents a valuable intangible asset that requires careful consideration during the acquisition accounting process. Accurately valuing and accounting for IPR&D is crucial for both the acquirer and investors to understand the true value of the acquired business and its potential for future growth. Understanding the accounting standards and best practices surrounding IPR&D can help ensure a successful and transparent acquisition process.

FAQ

- What is the difference between IPR&D and internally generated R&D?

- How is the fair value of IPR&D determined?

- Why is IPR&D expensed immediately upon acquisition?

- What are the implications of impairing IPR&D?

- How does IPR&D impact the financial statements of the acquiring company?

- What are some common challenges in valuing IPR&D?

- What is the future of IPR&D in business combinations?

Related Topics

- Business Combinations

- Intangible Assets

- Goodwill

- Impairment of Assets

- Financial Reporting Standards

Need support? Contact us at Phone: 0904826292, Email: research@gmail.com or visit us at No. 31, Alley 142/7, P. Phú Viên, Bồ Đề, Long Biên, Hà Nội, Việt Nam. We have a 24/7 customer service team.